{kind=link}

We’ve seen an easing in inflation this quarter which will have brought some relief to businesses and households, though not on housing costs. Output has continued to expand, including in the manufacturing sector, and business activity and optimism have held up. However, this has yet to feed through to consumer indicators – retail sales and household sentiment – and there are signs of a further slowdown in the expansion of the labour market.

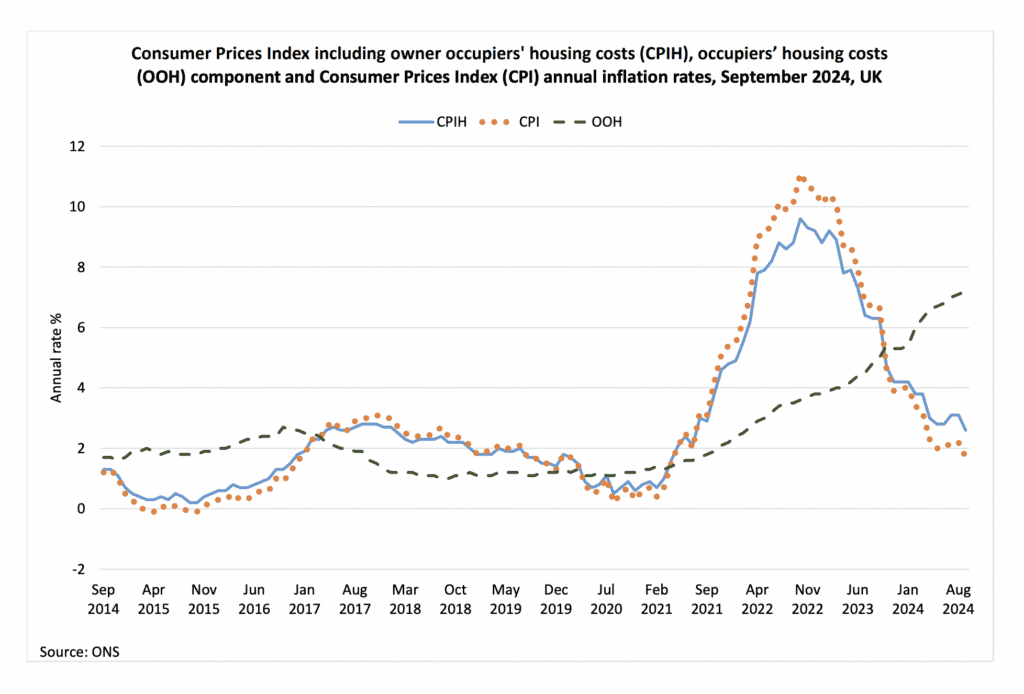

Inflation eases but housing costs still rising for renters and owners

After a slight rise in July and August, the UK rate of inflation has slowed. On the measure that includes owner occupied housing (CPIH), inflation rose just 2.6% in the 12 months to September, down from 3.1% in August, the lowest rate for over 3 years. The rate was also down month-on- month in August. The Consumer Price Index (CPI) rose by just 1.7% on an annual basis, down slightly on the 12 months to August (2.2%) and was largely unchanged on the September rate.

The most significant areas of downwards pressure on inflation on both measures was from the Transport sector with falling air fares and motor fuels, contributing to the largest annual fall since October 2015. Against this we saw a rise in food and non-alcoholic beverage inflation which rose 1.8% in the year to September making the biggest contribution to upwards pressure.

Communications costs also rose 5.2% year on year, and generally services price rises have been rising faster than goods over the past 12 months.

One in four Scottish employers continue to face worker shortages

One area where costs continue to rise steadily is housing, including costs for owner-occupiers, which rose in September on a 12-month basis for the 9th consecutive month by 7.2%, 0.6% on a monthly basis, and the highest rate since March 1992. But whilst owner-occupier costs have been going up, along with rents and council tax, the household energy component of household bills has fallen steadily over the past year.

November saw the second rate cut by the Bank of England this year, to 4.75%. However, although inflation has been coming down, the bank predicts a small further rise is inflation likely in the short term. This means we are unlikely to see another rate cut this year and a more gradual and cautious approach to further cuts over next year.

There was also little relief for renters. Private rents rose 7.2% in the twelve months to September in Scotland, slightly slower than in August (7.6%) and slower than the UK (8.4%) average. The general trend over the past year since the peak in August 2023 has been slowing rent inflation (note this is ONS experimental data and the Scottish data in this series are mainly for advertised new lets not subject to the price cap). The data also highlights the contrast across Scotland with average rents in Edinburgh topping £1,370 compared to Greater Glasgow at £1,190. RICS survey respondents note lower levels of new landlord listings in September in Scotland in contrast to tenant demand, leading to relatively robust expectations for rental rises for the quarter ahead.

UK house prices rose by 2.8% on an annual basis in August, up from July (1.8%) to £293,000. Prices rose by 5.4% in Scotland over the same period to an average £200,000, up on July, suggesting buyers this year are having to find an extra £10,000 on average to purchase (Note: the ONS note revisions due to uncertainty over new build prices are likely).

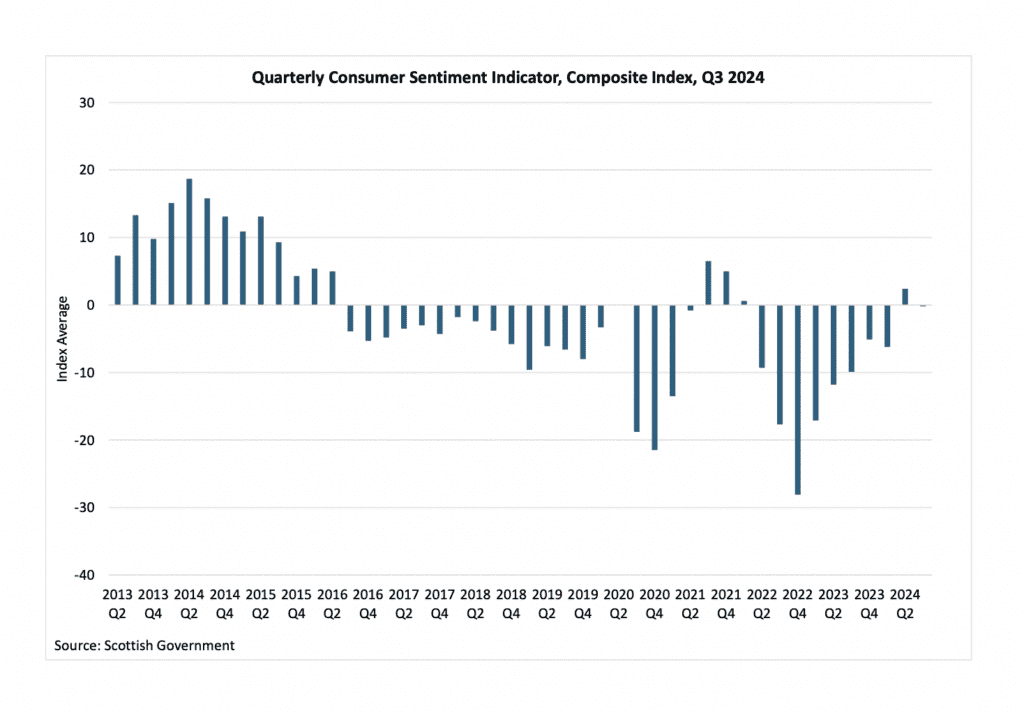

Consumer sentiment dips again after a brief rise

Scottish Consumer Sentiment was slightly negative in the third quarter of this year, decreasing by 2.6% on the previous quarter, and following the first rise in nine quarters according to Scottish Government (in experimental) data. However, it is still slightly stronger than the quarterly average and despite the fall is the second highest level since the beginning of 2022. The main reason for the fall was a weakening in the outlook of consumers for the coming year. Households expect their finances to worsen and although they expect the economy to improve, this is by less than last quarter.

This weaker sentiment is reflected in data from the high street. Data from early October from the Scottish Retail Consortium showed October sales rising by a marginal 0.1%, continuing what they describe as ‘static’ trading since the summer. Food sales were down slightly, which may reflect the effect of lower inflation offset by other non-food purchases.

Business optimism and activity holds up

The latest Royal Bank of Scotland Regional Growth Tracker showed private sector business activity in Scotland in September continuing to expand for the ninth consecutive month although at a slowing rate, as services growth slowed. Both rates of business activity and growth lagged the UK trends, with the rates of new business expansion amongst the lowest in the UK and drop in new orders for manufacturing. After a sustained period of expansion, the rate of job creation was above average, hitting a 16-month high, although with new activity slowing this rate of expansion may not be sustained.

Sentiment among firms responding to the Fraser of Allander Institute/Addleshaw Goddard’s Scottish Business Monitor in Q3 also remained positive. Expectations for business activity over the coming 6 months have held up at similar levels to Q2 and remain higher than the 2023 average and employment was one of the strongest indicators. Fewer businesses are reporting their costs have gone up. Employee costs remain the biggest concern, but the recent interest rate cut has relieved pressure on borrowing costs and appears to have boosted capital investment intentions although the balance of these remained negative.

Labour market conditions soften

Despite strong survey data, official data for the labour market suggests job creation is slowing in Scotland. The number of payrolled employees in Scotland remained unchanged in October relative to the same month a year ago. This represents the end of a three-year expansion, based on this experimental HMRC PAYE data (which is subject to revision). The rate of growth in the UK is on a similar slowing trend (0.3%). That said there are of course regional differences with Falkirk, Inverness & Nairn and Glasgow seeing above average rises in payrolled employees in October.

The claimant count unemployment rate rose in October in Scotland to 4%, a small rise on both the previous month and on the same month last year. The UK rate also rose to 4.7%. In historical terms these rates remain low but do suggest a softening in labour market conditions. The employment rate based on Labour Force Survey data (which should still be interpreted with caution due to sampling constraints), remained largely unchanged in the period at 73.7% relative to a UK rate of 74.8%.

However, but there was a very small rise in the percentage of people who were inactive, which rose to 23.7% creating further divergence with a falling UK rate, which fell to 21.8% in the period.

Recruitment indicators have also stabilised with the number of on-line job adverts returning to pre- pandemic levels. One in four Scottish employers continues to face worker shortages in October according to Scottish Government Business Insights and Conditions Survey (BICS). In a slight change the sector seeing the most acute shortages was hospitality (Accommodation and Food Services) with 31.9% seeing shortages followed by Admin and Support Services businesses (30.1%) and Manufacturing (28.7%).

Median monthly pay accelerated in October to by 7% in the UK, on an annual basis, ahead of inflation. This is a bigger increase than we have seen in recent months and reflects public sector pay rises particularly in the health and social care sector (including pay backdated to April). In contrast the ONS report the lowest rise was in the Public Admin and Defence sector. Pay in Scotland on the same measure rose by 6% in October on an annual basis and rose slightly faster than in September.

Growth continues in Scotland boosted by manufacturing and services expansion

Early estimates of UK GDP in September (subject to revision) show the economy growing for a third consecutive quarter but at a slower rate of 0.1%. Whilst an expansion in construction output boosted growth, a 0.2% fall in production output, including a 2.7% decline in electricity, gas, steam and air conditioning supply partially offset this. On a positive note, there was a rise in manufacturing output with roughly half of manufacturing sectors increasing output. The services part of the economy expanded by just 0.1%. There was no growth in business-facing services and just marginal growth (0.5%) in the consumer facing sectors e.g. wholesale and retail trade.

Scottish onshore GDP expanded by 0.4% in the second quarter of this year, underpinned by an expansion of 1.1% in production, including rising manufacturing output and 0.3% growth in services. In contrast to the UK trend the construction sector contracted slightly as did the wholesale and retail trade sector (though note this is the latest data available for an earlier quarter).

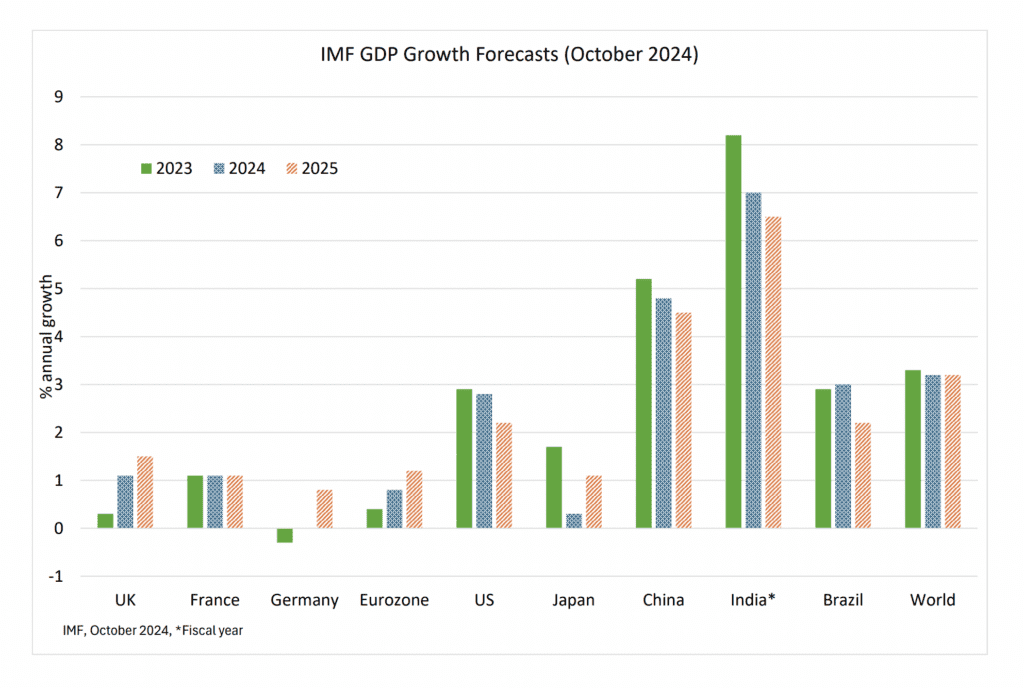

At the time of writing most forecasters had not yet updated their models to take account of the UK October budget. The Office for Budget Responsibility forecasts published with the UK budget forecast predict the UK economy expanding but at relatively modest rates of 1 % this year, 2% in 2025 and 1.8% in 2026. In their most recent publication, published pre-UK budget, the Fraser of Allander Institute forecast Scottish GDP at slightly lower rates, 0.9%, 1.1% and 1.2%. These are likely to be revised considering both budgets.

UK GDP of 0.1% in Q3 puts us behind the Eurozone (0.4%), Germany (0.2%) and US (0.7%) according to the IMF’s October forecasts. However, in their assessment, published on the 24th of October, they suggest the UK could grow ahead of the Eurozone average next year, but behind the US economy.

Economic analysis in association with Prosper.